Overview

The Exact Investment Philosophy I Use With My Millionaire Clients

This post walks through the exact investment framework I use with clients, from how we assess risk tolerance to the ETF-based portfolios we build. It explains why we avoid investing short-term money, why low-cost diversified ETFs are our core building blocks, and how time in the market matters more than chasing hot strategies. You’ll see sample portfolios using funds like VTI, VXUS, BND, and BNDX across five risk profiles, plus when a 100% stock portfolio can make sense. The goal is to give you a transparent look at how a fiduciary planner actually makes portfolio decisions, without the usual jargon or sales pitch.

Published on

Read Time

9 mins

Every day, there's a new investment strategy someone's trying to sell you. A new philosophy. A new thing that's going to change everything.

Honestly? Most of it is doing more financial damage than good.

So I figured I'd just pull back the curtain and show you exactly what I do with my own millionaire clients, including the risk tolerance questionnaire I use, the philosophy behind every decision, and the actual funds and allocations that make up each portfolio. Nothing held back.

While I use this same framework with a lot of my higher‑net‑worth clients, it’s the same philosophy I use across the board, tailored to each person’s situation.

Let's get into it.

First Thing I Do: Risk Tolerance

Before anything else, every client fills out a risk tolerance questionnaire. I'm not just doing this to check a compliance box; I genuinely need to understand how someone is going to behave when things get ugly in the market.

Because things will get ugly. At some point.

And if you want access to this exact risk tolerance questionnaire, here it is:

Risk Tolerance Questionnaire

Hey, I did say “nothing held back.”

Now, take this question, for example:

Imagine the stock market dropped 25% in the last three months. The individual stock you own dropped 25% too. What do you do?

Sell everything

Sell some shares

Do nothing

Buy more

That question matters a lot to me. Because the biggest mistake I see people make — over and over — is selling during a downturn and locking in losses that didn't have to be permanent.

Something Morgan Housel Said That I Can't Stop Thinking About

A couple of years ago, I was at a conference and got to hear Morgan Housel speak. He wrote The Psychology of Money. If you haven't read it, what have you been doing? Go get a copy now. He said something I've repeated to clients probably a hundred times since:

My objective with investing isn't to maximize returns. It's to maximize the likelihood that I stay invested.

That's it. That's really the whole thing a lot of the time. Stay invested. Don't lock in your losses. Give time the chance to do what it does and let compounding work in your favor.

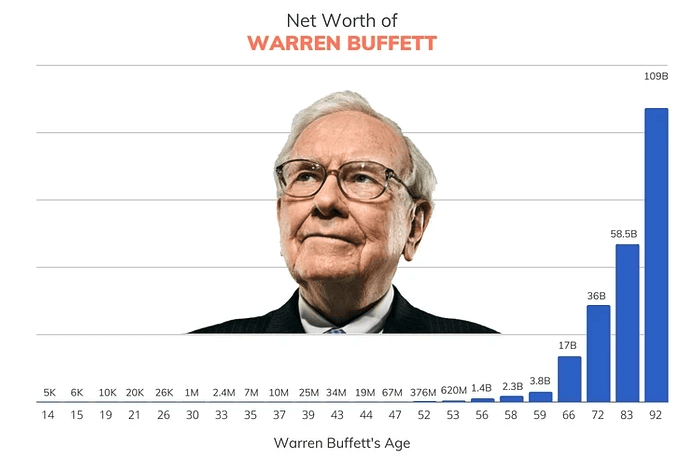

One interesting note, since we mentioned compounding. Did you know 99% of Warren Buffett's wealth came after he turned 50? Time in the market isn't a strategy. For a lot of people, it's THE strategy.

FinMasters: Warren Buffett’s Net Worth Over the Years

The Investment Philosophy (It's Simpler Than You Think)

Once I've got a read on someone's risk tolerance, we align on an investment philosophy. At my firm, that comes down to three things:

Low-cost ETFs

Allocation that matches your actual risk tolerance

Maximizing time in the market

Yeah, it really is that simple.

What About Goals That Are Only 2-3 Years Away?

As a general rule in our firm, we don’t invest money you’ll need in 2–3 years.

If you've got a goal that's 2 or 3 years out, such as a house down payment, a car, or a wedding, we're putting that in a high-yield savings account or a money market fund.

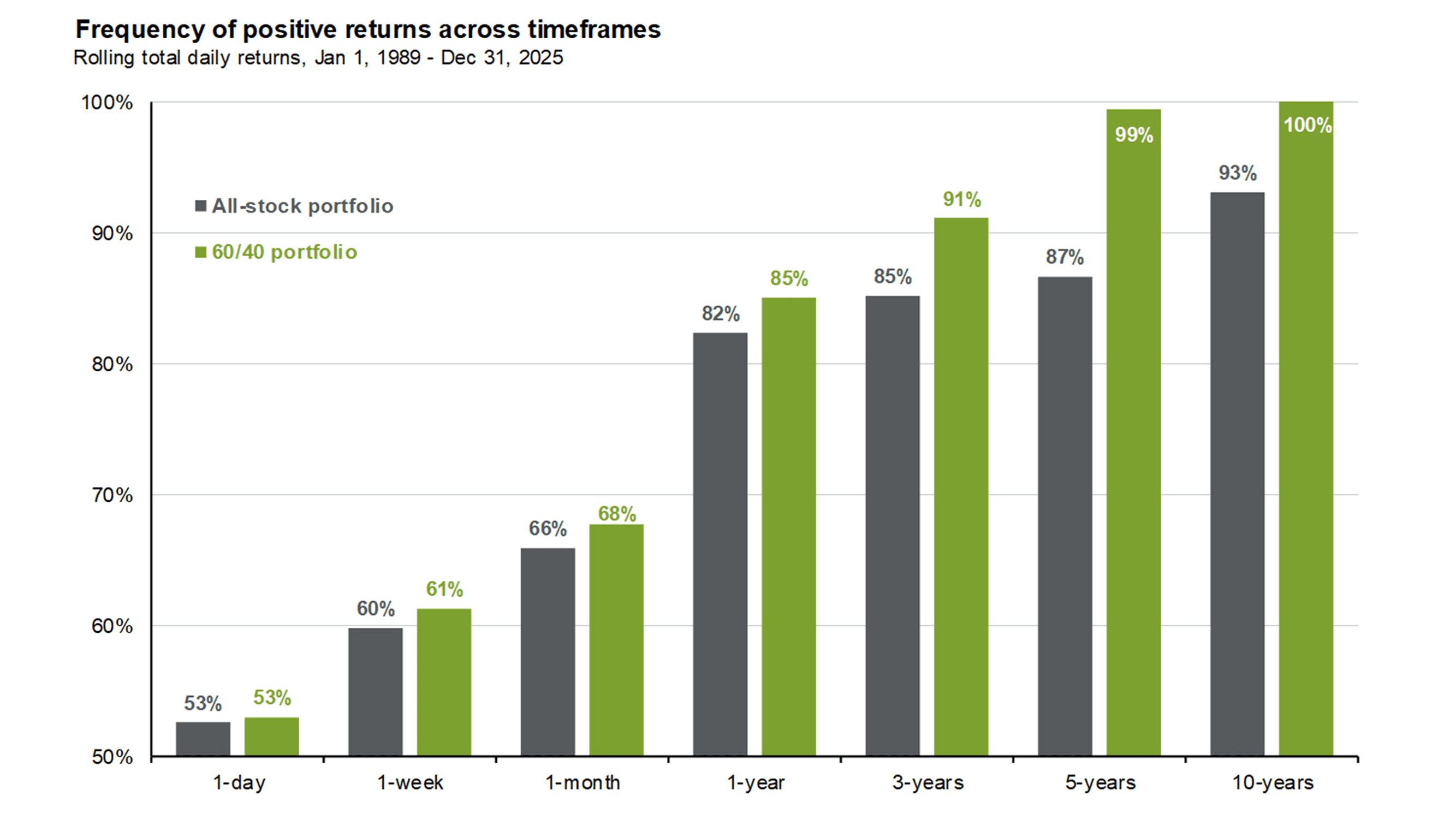

The reason for this is this chart right here:

JPMorgan: Guide To The Markets

As of March 2026, high-yield savings accounts and money market funds are getting about 3.5%, and when you think about the fact that an all-stock portfolio only had a positive return 82% of the time over any given one-year period (see the chart above)... the math just doesn't support the risk.

Save the market exposure for money you genuinely won't need for a while.

Which ETF Providers Do We Use?

Vanguard is our go-to. But honestly, there are a lot of great low-cost options out there — iShares by BlackRock, Charles Schwab. The thing they all have in common is low expense ratios, and that matters more than most people realize when you're compounding over 20 or 30 years.

The Exact Portfolio Allocations

Okay, here's where it gets specific. But we’ll use charts to try to make it easier to read. We use five risk profiles:

Aggressive

Moderately Aggressive

Moderate

Moderately Conservative

Conservative

Each one gets assigned a stock-to-bond split:

Risk Profile | Stocks | Bonds |

Aggressive | 100% | 0% |

Moderately Aggressive | 90% | 10% |

Moderate | 80% | 20% |

Moderately Conservative | 70% | 30% |

Conservative | 60% | 40% |

Time Horizon Matters Too

Here's something I want to flag because I see this get overlooked all of the time.

If you're 20 years old and saving for retirement 40 years away, sitting in an aggressive portfolio may make total sense. But if you're 65 and planning to retire next year and start pulling income from this thing? An all-stock portfolio probably doesn't make sense, regardless of how you answered the risk questionnaire.

Your time horizon and your risk tolerance have to work together. One doesn't override the other.

The Actual Funds We Use

Four funds. That's it. All Vanguard (but they don’t have to be, this is just what we use). Also, this is by no means a recommendation of what you should be using:

VTI — Vanguard Total Stock Market Index (U.S. stocks)

VXUS — Vanguard Total International Stock Market (international stocks)

BND — Vanguard Total Bond Market (U.S. bonds)

BNDX — Vanguard Total International Bond Market (international bonds)

The specific ETF weights shown here are our starting point models for each risk profile. Actual client portfolios can and do differ from these models based on individual circumstances, and nothing here should be taken as a recommendation for your situation.

Here's how those funds are weighted across each portfolio — heads up, there are a lot of numbers.

Risk Profile | VTI | VXUS | BND | BNDX | Total |

Aggressive | 60% | 40% | 0% | 0% | 100% |

Mod. Aggressive | 54% | 36% | 7% | 3% | 100% |

Moderate | 48% | 32% | 14% | 6% | 100% |

Mod. Conservative | 42% | 28% | 21% | 9% | 100% |

Conservative | 36% | 24% | 28% | 12% | 100% |

These are our standard model starting points; in practice, we customize based on taxes, existing holdings, cash needs, and client preferences, so actual portfolios can differ.

One more thing — we do have a portfolio that sits above aggressive at my firm. It's a 100% S&P 500 portfolio using VOO (again, not a recommendation, you can use what you're comfortable with). Less diversification, but for the right client with the right timeline, it's on the table.

To Wrap It Up

The best investment strategy is the one you'll actually stick with when the market drops 30%, and everyone around you is panicking.

Low-cost ETFs. An allocation that fits who you actually are. And time. That's the whole thing.

There's a lot more that goes into managing larger portfolios, rebalancing, tax considerations, and income planning in retirement. We'll get into all of that in future posts. But if you get the foundation right, the rest becomes a lot more manageable.

Cheers,

Common Questions

What is a risk tolerance questionnaire, and why does it matter?

It's a set of scenario-based questions designed to get a realistic picture of how you'd behave during a market downturn, not how you think you'd behave. It directly determines what kind of portfolio makes sense for you.

Is VTI better than VOO?

VTI tracks the total U.S. stock market — over 3,500 companies. VOO tracks the S&P 500 — the 500 largest. VTI gives broader exposure. VOO is a more concentrated bet on large-cap U.S. companies. Both are solid. The right one depends on your goals and how much diversification you want.

Should I invest money I'll need in two years?

With our clients, we avoid this. For anything under 3 years, the risk of a market downturn is too real. A high-yield savings account or money market fund is the smarter move in most, but not ALL cases. Right now, the rates on those aren't bad at all.

What's the right stock-to-bond ratio for my age?

There's no perfect universal answer. A 25-year-old saving for retirement in 40 years can take on a lot more stock exposure than someone two years from retirement who needs to start pulling income. Age matters, but so does your goal, your timeline, and how you'd honestly respond to seeing your account drop.

Why Vanguard ETFs specifically?

Mainly the cost. Vanguard has some of the lowest expense ratios in the industry, and when you're compounding returns over 20-30 years, fees that seem small start to add up to real money. That said, iShares, Schwab, and so many others have comparable options if you prefer those platforms.

The Boring Stuff (disclaimer):

This material is for informational and educational purposes only and is not individualized investment, tax, or legal advice. It does not take into account your specific objectives, financial situation, or needs, and it is not a recommendation to buy or sell any security or to adopt any particular investment strategy. The specific portfolios, allocations, and funds discussed are standard frameworks we use in most cases; actual client portfolios can differ based on taxes, existing positions, cash needs, and individual circumstances. All investing involves risk, including the possible loss of principal, and there is no guarantee that any strategy will be successful. Before making any financial decisions, you should consider your personal circumstances and consult with a qualified professional.

Tired of guessing With your money?

Book your free Financial Health Check, and we'll walk you through your biggest risks, hidden opportunities, and the exact next steps to get your money under control.