Overview

Is AI Actually Good Enough to Replace Your Financial Advisor? (Real Test)

AI built a 25-page financial plan in 10 minutes — and some of it was actually good. But buried inside were tax errors serious enough to cost someone thousands, missing strategies a self-employed person at $100K should never go without, and contribution recommendations that had absolutely no basis in the client's actual cash flow. The scary part isn't that AI got things wrong, it's that it got them wrong in ways most people would never catch.

Published on

Read Time

9 mins

A financial plan takes me upward of 20 hours to build for a single client.

AI did it in 10 minutes.

So naturally I asked: is the plan any good?

Spoiler — shockingly easy to do, and the results were a mixed bag. Parts of it were genuinely solid. Other parts were the kind of advice that could quietly cost someone real money if they followed it without pushback.

I went through the entire 25-page plan section by section — the same way I'd sit down with a client and review it — and I'm going to walk you through what held up, what didn't, and what it actually means for anyone asking whether AI can replace a real financial planner.

How I Did It

I used Claude Sonnet 4.6. ChatGPT and Gemini should be able to pull off something similar. I built a fictional client — Mark, 25, California — put together a detailed prompt with his financial info, and sent it off. If you want access to the prompt I used, here it is: AI Financial Plan Prompt.

Quick note before we get into it: don't put your real, personally identifiable information into any AI system. A fictional client works fine for testing. Real data is a different story.

What the AI Actually Got Right

I want to be fair about this. There were legitimately good sections.

Urgent Priorities

The opening laid out a clear list of things to act on right away. That's the right instinct. A financial plan shouldn't start with investment strategy — it should start with what needs to happen this week.

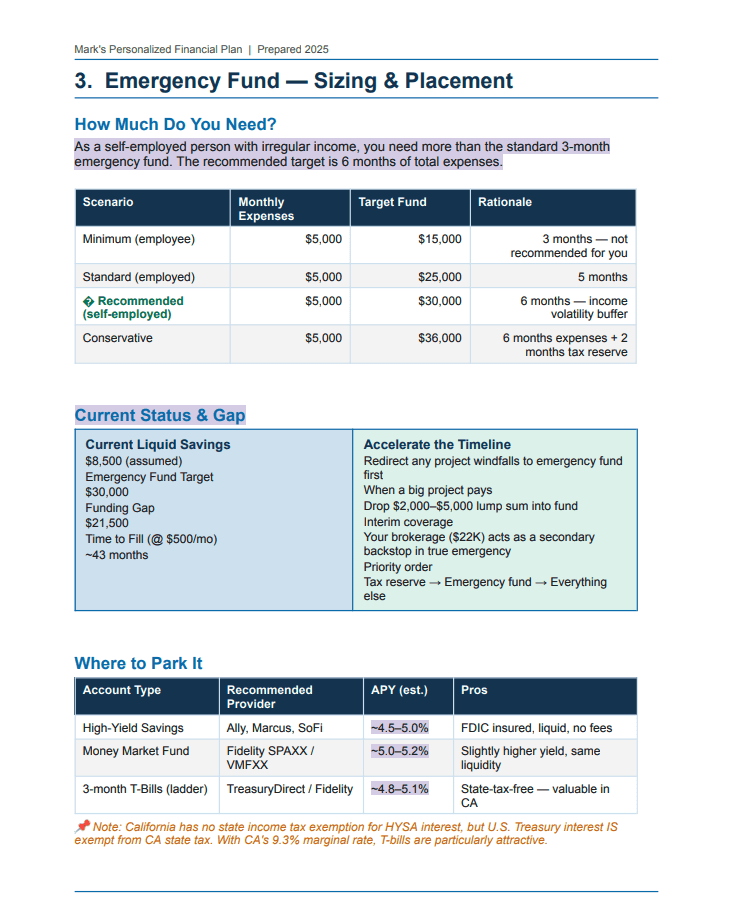

Emergency Fund Guidance

Starting at three months and working toward six — reasonable. The math was clean: drop in $8,500 now, contribute $500 a month, use lump sums from big projects to accelerate it. Nothing wrong with that.

One thing I'd push back on though. It lumped the buffer fund and the emergency fund together. In my opinion, those need to be completely separate accounts. The buffer fund is specifically for freelancers — it covers the slow months so you're not raiding your emergency fund every time a client is late. But that's a separate article.

Insurance Priorities

This one actually surprised me. It flagged disability insurance, brought up health insurance since the client was about to age off his parents' plan, and mentioned professional liability. All of that is exactly right for a 25-year-old freelancer. No notes.

Estate Planning Basics

Beneficiary designations. I say this to every single client and a shocking number of people still don't do it. The AI made it a priority and attached a real timeline to it — do this this week, do that within 30 days. That's how it should work.

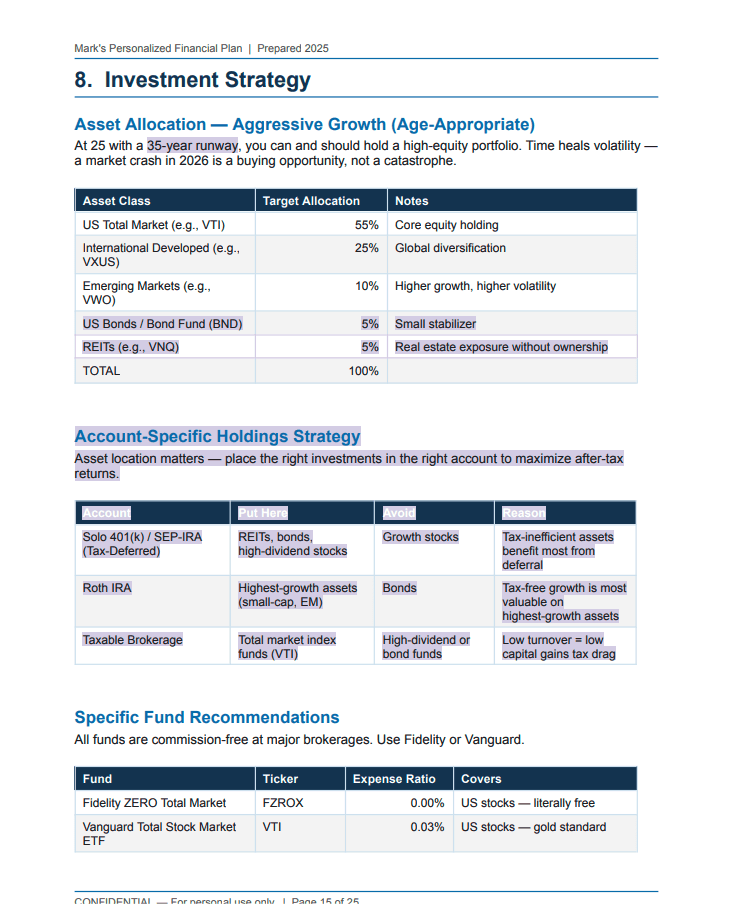

Account-Specific Investment Strategy

Honestly one of the best sections. Highest-growth assets in the Roth IRA since growth is tax-free. Bonds and REITs in tax-advantaged accounts so dividends don't trigger a taxable event right now. Taxable brokerage focused on tax-efficient funds. Textbook. Got it right.

Behavioral Guardrails

Automatic contributions. Remove the decision entirely so you're not relying on willpower every month. That's good behavioral finance thinking and it doesn't get talked about enough. The rebalancing piece had a problem — we'll get to that — but the concept of building guardrails into a plan is exactly right.

Where It Went Wrong

Here's where I have to be straight with you.

The High-Yield Savings Rates Are Outdated

The plan cited yields of 4.5 to 5% for high-yield savings accounts. That's not the current market as of March 2026. Rates have moved. AI trained on older data won't know that — and basing real savings goals on inflated yield assumptions will throw off the math on things that actually matter, like a house down payment.

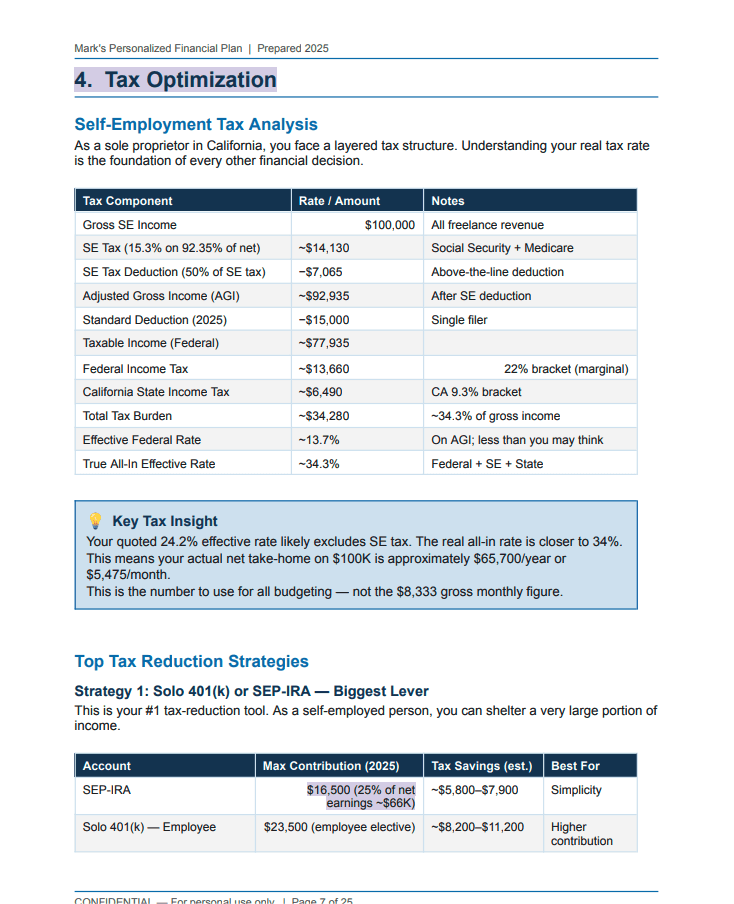

The Tax Section Was the Worst Part

I'll just be direct.

It told a sole proprietor they could contribute 25% of net earnings to a SEP IRA. The actual number for a sole proprietor is 20%. That's wrong.

Then it recommended $23,500 to a Solo 401k plus $7,000 to a Roth IRA in the same year. $30,500 in retirement contributions for someone with about $1,000 in monthly surplus who still hasn't funded his emergency fund or set aside quarterly taxes. I genuinely don't know where it thought that money was coming from.

It also estimated a 34% effective tax rate for someone making $100,000. If a client walked in with that number, the first thing I'd ask is who does their taxes. That rate at that income level is not realistic. Something went very wrong somewhere.

And the two things that actually could have helped this person the most — the QBI deduction and the S-corp election — weren't mentioned once. At $100,000 in self-employment income, electing S-corp status alone could save thousands a year in self-employment taxes. The AI skipped it entirely.

The Business Deductions Were Made Up

The plan estimated $2,000 to $5,000 for computers and equipment. $500 to $2,000 for software. No basis for either number. I specifically asked for specifics — and instead of asking a follow-up question, it just filled in wide ranges and kept moving.

If you don't have the information, ask for it. Wide-range guesses dressed up as financial planning aren't useful. They're noise.

Rebalancing With No Mention of Taxes

Annual rebalancing was the recommendation. Fine, in theory. But it didn't say anything about what rebalancing a taxable brokerage account actually does — which is potentially trigger capital gains taxes every single year if you're not being careful about how you do it.

There's a cleaner way to handle this. Direct new contributions proportionally so the allocation naturally drifts back without selling anything. In a Roth IRA or Solo 401k, rebalance however you want — there are no tax consequences. The plan treated every account the same. That's a meaningful oversight.

The Debt Payoff Logic Was Thin

Student loans at 4.5%. Historical market returns around 7%. The math is clear — invest the difference. The plan saw the same math, acknowledged it, and then told the client to pay off the debt anyway. The reason? The psychological freedom of zero debt.

Maybe that's the right call for some people. But it never asked whether this client actually feels burdened by the debt. It assumed he did. That's a real financial decision being made on a guess.

The Home Purchase Plan Missed the Five-Year Roth Clock

The client wanted to buy a house in five years. The plan mentioned the Roth IRA first-time homebuyer exception — up to $10,000 in earnings, penalty-free. Good. But it left out the thing that actually matters: there's a five-year clock. The Roth IRA has to have been open for five years before you qualify.

At 25, if he doesn't open one now, that exception isn't available when he needs it. The plan said nothing about this. That's not a minor footnote — it's the whole point of mentioning the exception in the first place.

What My Actual Client Plans Look Like

Here's what a real plan covers that this one didn't touch:

A values alignment survey — about 50 questions — so money decisions actually reflect what matters to the person, not just what the numbers suggest

Key financial health metrics: emergency fund coverage, debt rate, burn rate, savings rate, net worth trend over time

A full tax sheet with actual federal and state calculations — not a range, a real number — and exactly how much to set aside each quarter

Tax diversification across pre-tax, Roth, and taxable accounts, which is especially important for anyone thinking about early retirement

An investment sheet showing current allocation vs. recommended allocation, and how the portfolio has tracked against its benchmark

A buffer fund kept completely separate from the emergency fund — built specifically for variable income so a slow month doesn't become a crisis

A cashflow summary broken into four buckets: grow, debt, live, tax

A surplus plan that recalculates every time a goal gets hit and redirects those funds to whatever's next

That's what 20 hours buys you. Not just a document — a plan that actually knows who you are.

So Is an AI Financial Plan Worth Anything?

Honestly, for the right person in the right situation — maybe.

If you're just starting out, your finances are simple, and you need a basic framework to think through? An AI plan can be a reasonable place to start. Something to react to.

But the moment real complexity shows up — self-employment, a business, significant assets, a major transition — the gaps stop being theoretical. The S-corp election. The QBI deduction. The five-year Roth clock. The rebalancing tax trap. None of those are unusual edge cases. They're normal situations. The AI missed all of them.

Is AI Going to Replace Financial Planners?

I get asked this constantly. And I'm genuinely not worried.

A financial planner isn't someone who runs numbers. The job is to step into a person's financial life, figure out what they actually want, hold them to it, and be there when things get complicated. AI doesn't do that. Not yet.

Think about Best Buy. When Amazon launched, everyone said Best Buy was finished. It wasn't. Because people still wanted to walk into a store, talk to someone who knew what they were talking about, and get a real opinion before spending real money on something that mattered.

Same thing applies here. The stakes are just a lot higher than a TV.

The Bottom Line

A 25-page financial plan in 10 minutes. Some of it was solid — the implementation timeline, the insurance priorities, the account-specific investment strategy were all good.

But the tax math was wrong. The most valuable strategies for a self-employed person weren't mentioned. Expense numbers were made up. And the contribution recommendations didn't come close to matching the client's actual cash flow.

Use it as a thinking tool. Don't use it as a plan.

If your situation has any real complexity to it, talk to a CFP or a CPA. What you pay them will come back to you.

Cheers,

Can AI create a real financial plan?

It can create something that looks like one. A well-prompted AI will produce a structured, detailed document. But it works from assumptions, can't ask follow-up questions the way a human advisor would, and tends to miss situation-specific strategies, especially around taxes and self-employment.

What do AI financial plans get wrong?

In the test I ran, the biggest errors were in the tax section: wrong Solo 401k contribution limits for a sole proprietor, an unrealistic effective tax rate estimate, missing the QBI deduction, missing the S-corp election opportunity, and recommending contribution amounts the client couldn't actually afford based on their cash flow.

Is it safe to use AI for financial planning?

For simple situations — basic budgeting, a debt payoff framework — it can be a reasonable starting point. For anything involving self-employment, significant assets, tax strategy, or major life transitions, you need a human who can ask the right questions and be accountable for the advice they give.

What does a real financial plan include that AI misses?

A real plan includes values alignment, precise tax calculations by state and federal bracket, a buffer fund strategy for variable income, a tax diversification plan across account types, rebalancing strategies that account for capital gains, and a surplus plan that adjusts as goals are achieved. It also includes a human who knows you and can hold you accountable.

Will AI replace financial planners?

Not the way most people think. The core value of a financial planner isn't calculating numbers — it's understanding a specific person's situation, making judgment calls when the math alone doesn't give you the answer, and being present as an accountability partner over time. That part of the job isn't going away.

The Boring Stuff (disclaimer):

This material is for informational and educational purposes only and is not individualized investment, tax, or legal advice. It does not take into account your specific objectives, financial situation, or needs, and it is not a recommendation to buy or sell any security or to adopt any particular investment strategy. The specific portfolios, allocations, and funds discussed are standard frameworks we use in most cases; actual client portfolios can differ based on taxes, existing positions, cash needs, and individual circumstances. All investing involves risk, including the possible loss of principal, and there is no guarantee that any strategy will be successful. Before making any financial decisions, you should consider your personal circumstances and consult with a qualified professional.

Tired of guessing With your money?

Book your free Financial Health Check, and we'll walk you through your biggest risks, hidden opportunities, and the exact next steps to get your money under control.