Overview

The One-Page Financial Plan Built for Freelancers and Content Creators

Most financial advice was built for people with one employer and one paycheck — not for freelancers and content creators juggling variable income, multiple revenue streams, and quarterly taxes. The one-page financial plan fixes that by breaking your entire financial picture down into five sections: cash flow and net worth, taxes, investments, risk analysis, and a 12-month action plan. It takes 1 to 2 hours the first time through and about 45 minutes every year after that. Come back to it once a year and you'll always know exactly where you stand and what to do next.

Published on

Read Time

9 mins

This is the one-page financial plan. It consists of five sections, all of which are completable in 1 to 2 hours, and is built to give you a clear picture of where your money stands and what to do about it.

Why One Page?

Because complexity is the enemy of action.

Most financial plans consist of 30-40 pages of random graphs and charts that no one cares about. This one only takes a single page, front and back. You can update it once a year in just 45-60 minutes. And it covers most things that actually matter.

The 5 Sections of the One-Page Financial Plan

Section 1: Cash Flow and Net Worth

Section 2: The Tax Sheet

Section 3: The Investment Sheet

Section 4: The Risk Analysis

Section 5: The Next 12 Months Action Plan

Let's go through each section now.

Section 1: Cash Flow and Net Worth

This is where most freelancers have no idea where they actually stand. And until you know the real number, everything else is a guess.

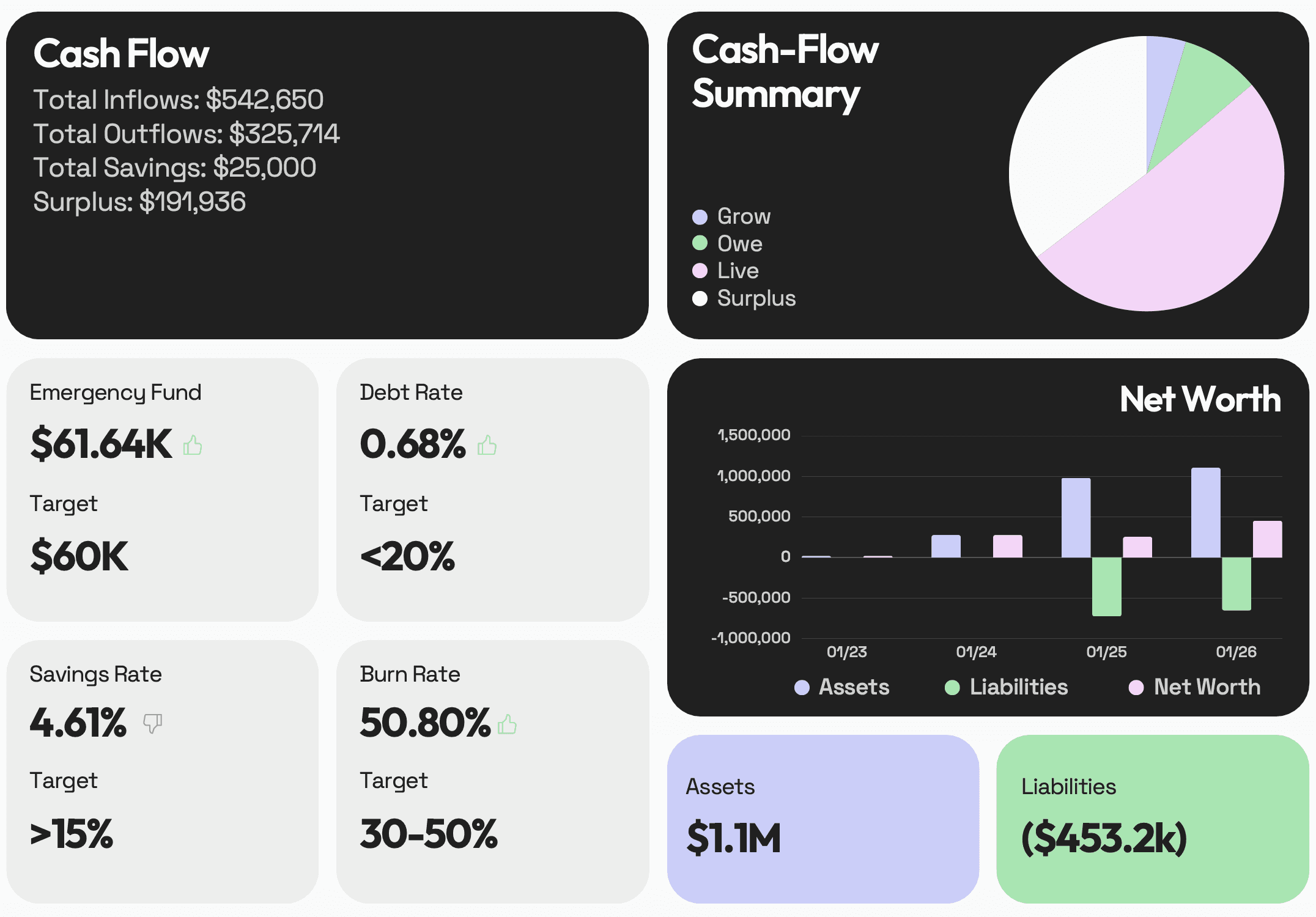

The Cash Flow Block

You need 4 numbers:

Total inflows — this is everything coming in: client payments, brand deals, affiliate income, interest, dividends, etc.

Total outflows — this is everything going out: rent, software subscriptions, food, equipment, coffee, etc.

Total savings — money already going somewhere intentional: a Roth IRA, a savings account, a tax reserve

Monthly surplus — inflows minus outflows (and money already being saved).

Your monthly surplus matters the most because it tells you exactly how much you have left to work with at the end of every month. For a content creator, this number swings. That's normal. The goal is to know what it looks like on average — not just in your best months.

The 4 Financial Health Indicators

These four metrics give you an honest read on where your finances actually are right now.

Metric | How to Calculate It | Target |

Emergency Fund | Non-discretionary monthly expenses x 3–6 | 3–6 months minimum |

Debt Rate | Total monthly debt payments ÷ total monthly income | Under 36%, ideally under 20% |

Savings Rate | Total monthly savings ÷ total monthly income | Above 25%, 15%+ is solid |

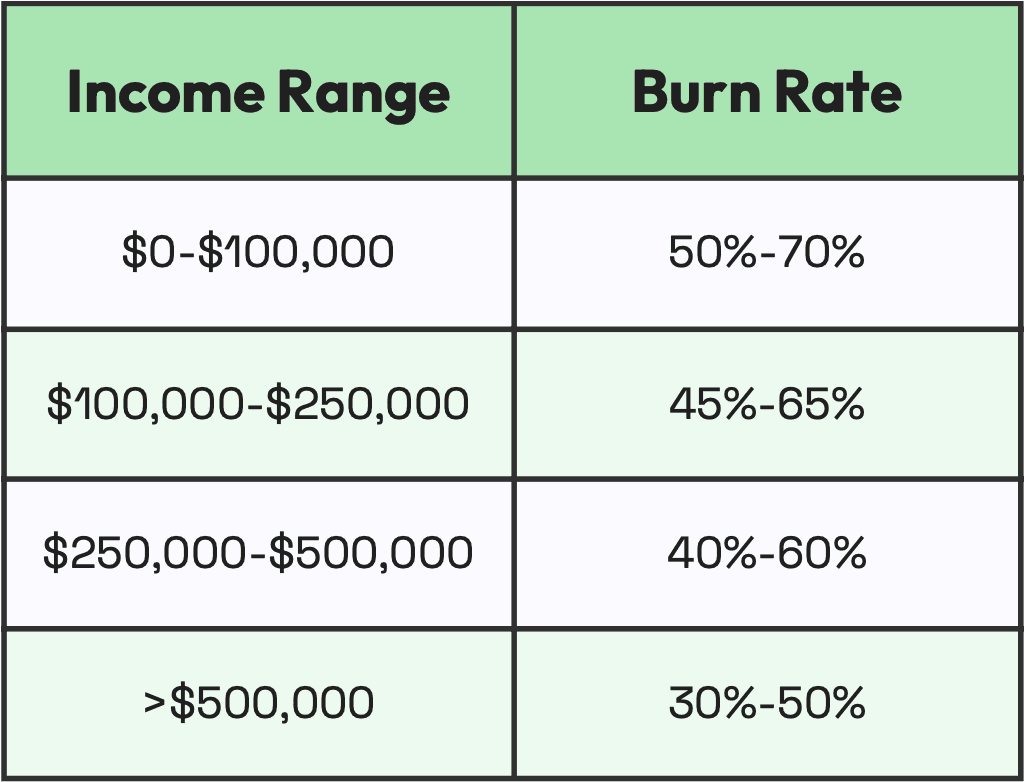

Burn Rate | Total monthly spend ÷ total monthly income | Depends on income range — see chart below |

A quick note on the emergency fund for freelancers specifically: the standard 3-month rule wasn't designed for variable income. If your revenue is unpredictable month to month — and for most content creators it is — lean toward 6 months. And consider keeping a separate buffer fund on top of this to cover slow months without touching your emergency savings. That's a separate account, separate purpose.

Net Worth

Assets minus liabilities. What you own minus what you owe.

Track this once a year — late January or early February works well once your year-end statements are out. Watching this number grow over time is one of the most motivating things you can do for your financial life.

Section 2: The Tax Sheet

This is the section that most freelancers and content creators skip. It's also the one that causes the most financial pain when ignored.

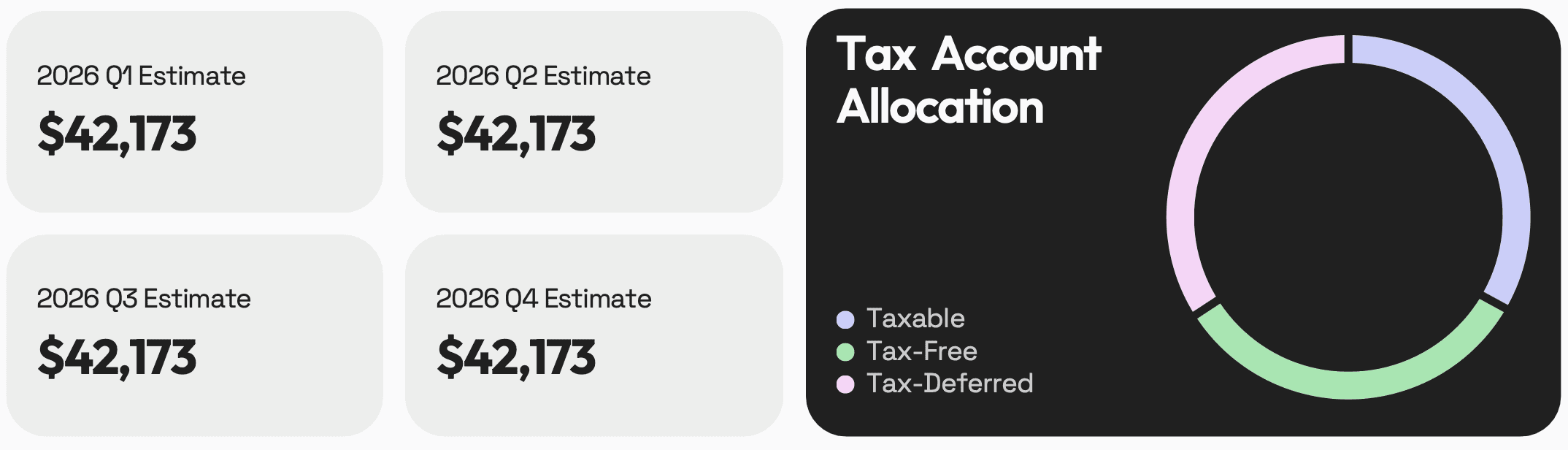

Current Year Tax Estimate

If you're a W-2 employee somewhere, your employer handles most of this. But if you're self-employed, you need to know your estimated tax bill before the IRS sends you a surprise.

A rough rule of thumb: set aside 20 to 30% of your self-employment income for taxes. But rough is the keyword there. The actual number depends on your deductions, your state, your filing status, and whether you've made any retirement contributions. A CPA who works with self-employed creators can get you to a real number — and the difference between a rough estimate and a real one is often significant.

Tax Diversification

This one doesn't get talked about enough.

The goal is to have money spread across all three types of accounts.

Taxable accounts — regular savings and brokerage accounts. You pay taxes on gains when you sell.

Tax-free accounts — Roth IRA, HSA. You contribute after-tax dollars and pay nothing on the growth.

Tax-deferred accounts — traditional 401 (k), traditional IRA. You get the tax break now and pay later in retirement.

For freelancers and content creators planning to retire early or wanting flexibility in retirement, tax diversification isn't just nice to have. It's one of the most powerful tools you've got.

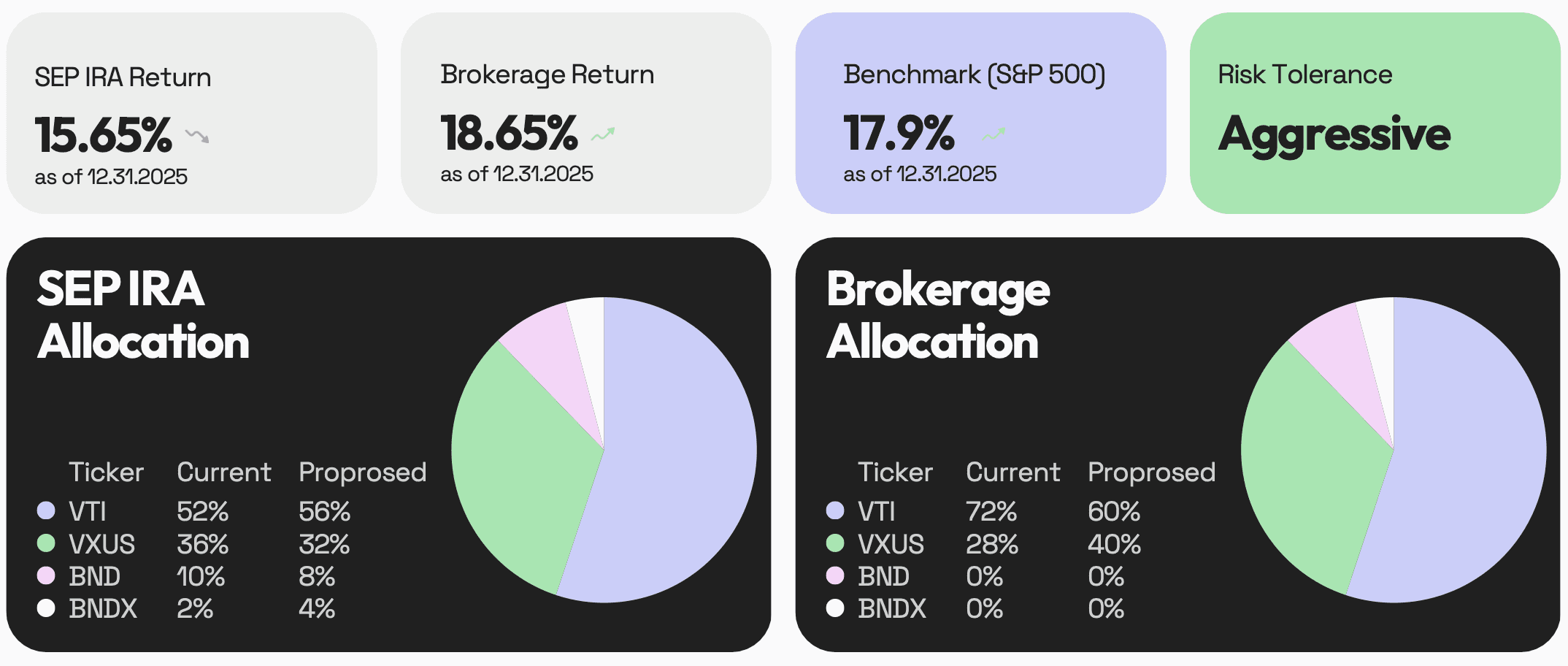

Section 3: The Investment Sheet

Two things. That's all this section needs.

Your Returns vs. Your Benchmark

How did your investments perform this year compared to whatever benchmark you're tracking against? If you're happy with the gap, move on. If you're not — that's a bigger conversation about your overall investment strategy.

Current Allocation vs. Target Allocation

Over time, markets move, and your portfolio drifts. A stock that was supposed to be 60% of your portfolio might now be 70% because it ran up. This section is where you catch that and decide whether to rebalance.

One thing worth knowing: in most cases, rebalancing inside a retirement account like a Roth IRA or 401k has no direct tax consequences. Rebalancing inside a taxable brokerage account is different — selling anything at a gain triggers capital gains tax. Be careful there.

Section 4: The Risk Analysis

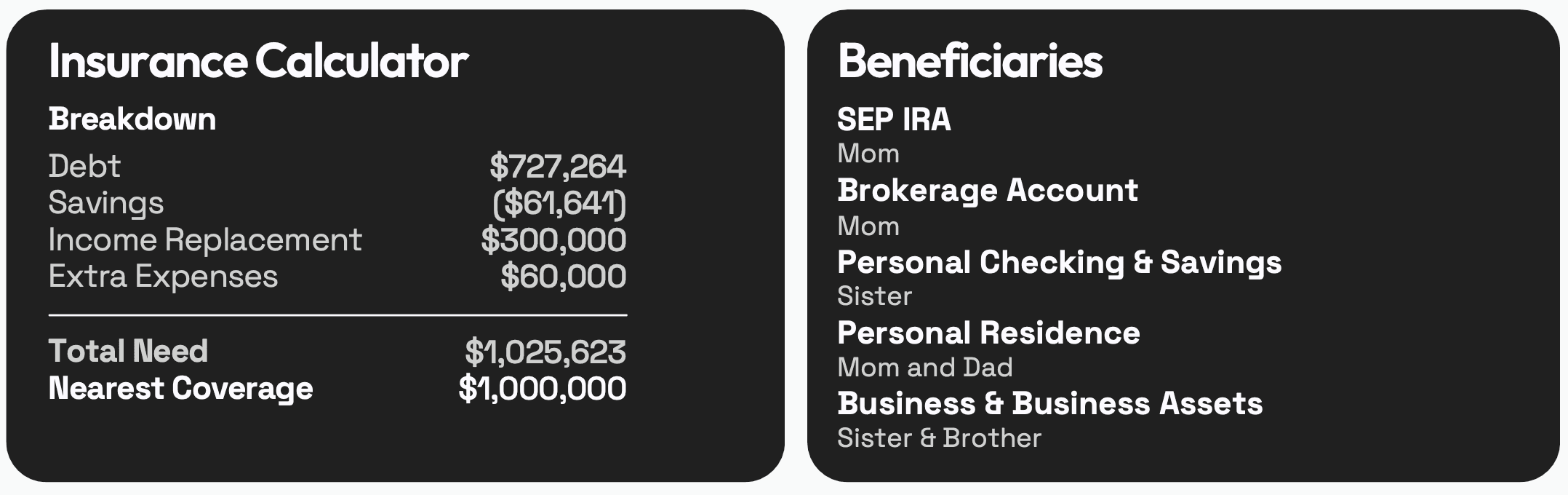

The Life Insurance Calculator

This is simpler than it sounds. The calculator answers one question: Do you actually need life insurance this year, and if so, how much?

The formula: total debt, minus total savings, plus income replacement (for whoever depends on your income), plus final expenses. That gives you a number to compare against whatever coverage you currently have.

The Beneficiary Check

This takes five minutes, and most people never do it.

Log into every account that has a beneficiary designation, such as retirement accounts, life insurance, bank accounts, and confirm the names are current. Outdated beneficiaries have caused enormous problems for families. An ex-spouse, a deceased parent, or no one listed at all. It happens more than you'd think. Check it once a year.

Section 5: The Next 12 Months Action Plan

This is where everything you just learned turns into something you actually do.

After going through all four sections, you'll have a list of things that need to happen. Maybe you're underinsured. Maybe your emergency fund is short. Maybe your investment allocation has drifted and needs a rebalance. Maybe you've never set up a tax reserve account, and your quarterly estimates are a mess.

Write it all down here. Give each item a timeline. This is your financial to-do list for the year.

At the end of the page, add your current goals. The ones you're tracking, the new ones you're adding. The whole point is to check in on these every year and see if you're on track.

How Long Does This Actually Take?

The first time through: 1 to 2 hours. Especially if you've never tracked any of this before and you're hunting down account numbers and statements.

It should only take 45 minutes to one hour every year after that.

One to two hours once a year to have a complete picture of your financial life. For most people, that's a better return on time than anything else they'll do this year.

The Bottom Line

Financial planning got overcomplicated somewhere along the way. And for freelancers and content creators, people with variable income, multiple revenue streams, and no HR department handling any of this, that complexity is a real barrier.

This plan cuts through it.

Cheers,

Do freelancers need a financial plan?

More than most people, yes. Variable income, quarterly taxes, no employer-sponsored benefits, and multiple revenue streams all create complexity that a standard financial plan doesn't address. A plan built for your situation — even a simple one-page version — makes a significant difference.

How do content creators manage irregular income?

The key is building systems around your average income, not your best month. That means calculating your monthly surplus based on a rolling average, keeping a buffer fund separate from your emergency fund to cover slow months, and setting aside taxes as income comes in rather than waiting until Q4.

What savings rate should a freelancer aim for?

Anything above 25% is strong. Above 15% is solid. The challenge for freelancers is that the savings rate looks different every month — which is exactly why tracking an annual average matters more than obsessing over any single month.

How much should freelancers set aside for taxes?

A rough rule of thumb is 20 to 30% of net self-employment income. But the real number depends on your deductions, your state tax rate, and your filing situation. A CPA who works with self-employed people will get you closer to an accurate number — and that precision is usually worth the cost.

What is tax diversification and why does it matter for freelancers?

Tax diversification means having money spread across taxable, tax-free, and tax-deferred accounts rather than concentrated in just one type. For freelancers — especially those planning to retire early or wanting flexibility — this gives you control over your tax bill in retirement rather than being locked into one tax treatment.

How often should I update my financial plan?

Once a year is enough for most people. Late January or early February works well — year-end statements are out and you have a clean picture of the previous year. Major life events like a significant income change, a new business, or a home purchase are also good reasons to revisit it outside of the annual review.

This blog is for educational purposes only and does not constitute financial, tax, or legal advice. Individual circumstances vary. Consult a qualified financial planner or CPA before making financial decisions.

Tired of guessing With your money?

Book your free Financial Health Check, and we'll walk you through your biggest risks, hidden opportunities, and the exact next steps to get your money under control.